Suppose you have learned or designed an EV+ strategy thoroughly tested which satisfy all the requirements to be considered the core of a winning system. You might think you are now ready to trade; you have clearly defined the rules to open and close trades, but then you wonder: how should I size my trades? At this point, most traders have read some generic stuff about money management. Ideas such as “you should put on risk no more than 1% of your balance in a single trade” are followed by many traders. Others are aware of the concept of drawdown and apply some formula based on that. Finally, some traders size their trades somehow according to their previous experience. Are these ideas, or any similar, right? Are they valid for any strategy? Are you optimally exploiting your balance, or even more important, is your balance safe?

Variables involved

In order to determine the trade size for your strategy, you have to take into account the following:

- Variance of your strategy

- Trade warranty required by your broker

- Number of simultaneously opened trades

The first point is often considered – despite wrongly or suboptimally in many cases -. You know your strategy has periods where it is lossing, and you must size your trade in such a way that your balance tolerates them. It is critical to have a large historical strategy backtest in order to have a confident estimation of its variance.

The second point leads to a conclusion of which most traders are not aware: your trade size also depends on your broker’s conditions! Your trade size cannot be the same when trading with futures, where warranties working with indices are usually around 10%, than when trading with CFDs, where warranties are much lower. In the first case, a trade size which would be suitable if working with CFDs might prevent you from opening a new position requested by your strategy, even when your balance perfectly affords it.

The third point is strategy and broker dependent. On one hand your trade size must allow you to open as many simultaneous trades as your strategy requires; on the other hand, your trade size must take into account whether your broker allows longs and shorts warranty compensation over the same asset.

Finding the optimal trade size

Strategies may differ in many ways from the point of view of money management. Does your strategy require to keep long and shorts over the same asset at the same time? How many trades shall be simultaneously opened? Does it have fixed stop loss and take profit or not? Since many variables are involved, the best way to find the optimal trade size is to run simulations of your strategy with different trade sizes until the highest one which satisfies all the conditions enumerated before is found.

I made an analysis considering the following system and broker features:

- Strategy standard deviation: 1.36

- Simultaneous longs and shorts over the asset compensate for the warranty

- Net simultaneous positions (avg±std dev; peak): 10.3±10.5; 68

- Warranty: 1%

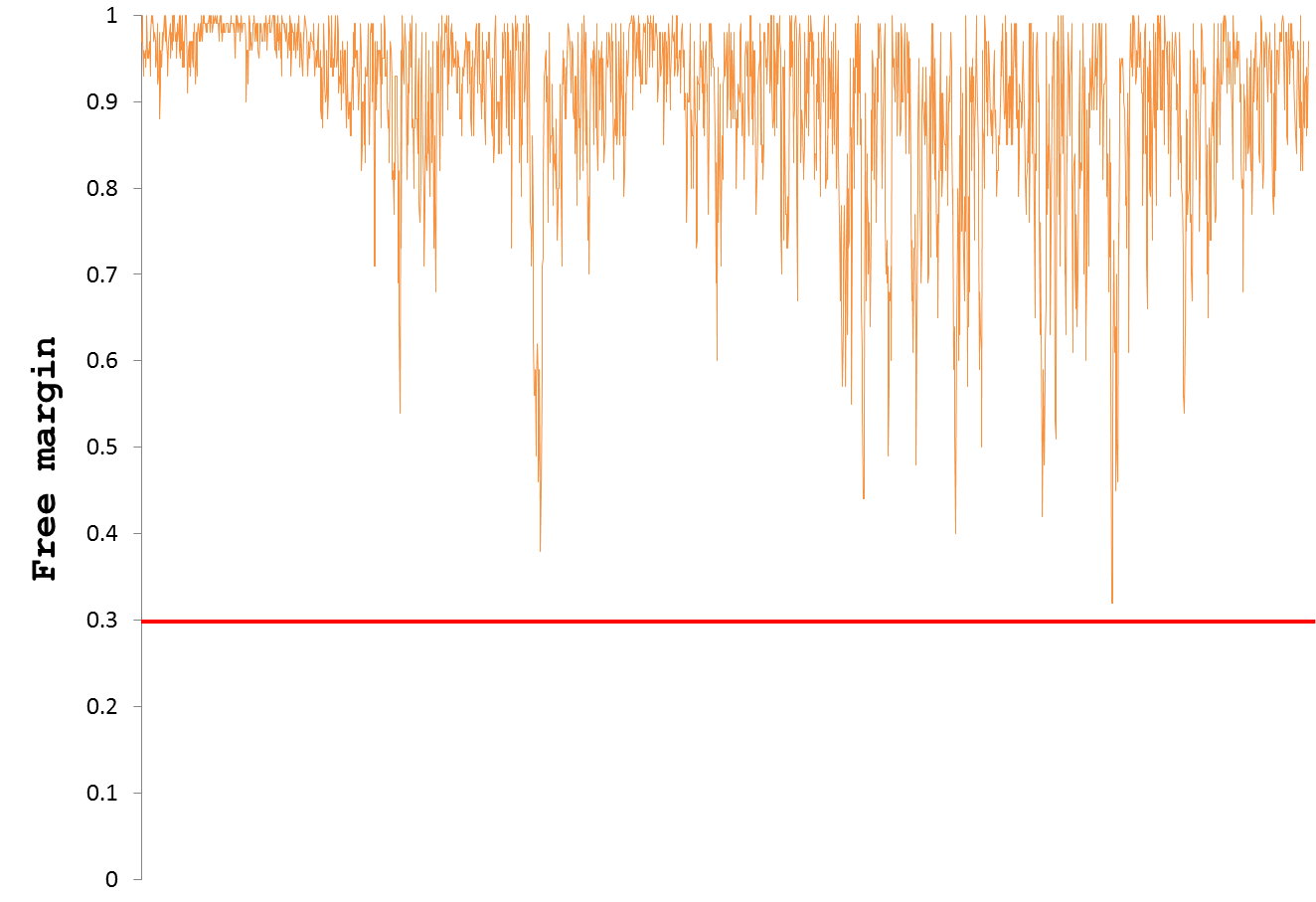

- Margin threshold: 30%

I ran simulations initiallly setting the trade size as account balance / warranty, and then iterating decreasing the trade size until a value satisfies the conditions along the whole simulated sample. The initial value will definitely fail in several ways since it obviously does not tolerate the system variance and it cannot support more than one net long/short, but it is just a starting point, and computations only takes a few minutes.

The graph below shows the highest trade size value which succesfully passed the test.

And this other graph shows the inmediatly higher value which fails. The square marks the point where margin falls below our threshold and therefore the simulation is aborted.

Impact of suboptimal trade sizes

What about if we are trading with trade sizes far from the optimal? There are two scenarios:

a) Trade sizes higher than the optimal

The consequences in this case depend on how far from optimal the trade size is, and how we face big swings (and not only losses, we should also be concerned about huge winnings!). Trade sizes very far from the optimal will likely end busting our account. This is sadly common between amateur traders who turn leverage into a massive destruction weapon. If our trade size is just a bit far from the optimal, we will find situations where our margin does not allow us to open a trade required by our strategy. This situation is obviously much less harmful than the previous one, but it should be considered as a serious warning. We should inmediately review our money management.

b) Trade sizes lower than the optimal

Trades sizes lower than optimal cause a performance degradation as a result of a too conservative leverage. This conclusion is intuituve, but the quantitative aspect is not so intuitive. The last graph depicts the impact of choosing too low trade sizes. Data are normalized to the optimal value. We can see how the performance logarithmically decreases, where, for example, a trade size only a 10% lower than the optimal leads to just a 37% the performance of the system with the optimal trade size.